Digital Banking Guide 2026: The Ultimate Beginner’s Handbook

Somewhere in India today, someone will make their first UPI payment — probably taught by a child or grandchild, probably nervous about pressing the wrong button. If that’s you (or someone you love), this digital banking guide is written for you. No jargon, no assumptions — just the five things every new digital banking user must know in 2026.

Table of Contents

1. Start With the Right Setup

- Use only official apps: your bank’s own app, or established UPI apps (PhonePe, Google Pay, Paytm, BHIM) downloaded from the Play Store/App Store — never from a link someone sends you.

- Register your own SIM: UPI ties to the mobile number registered with your bank account. That SIM must be in the phone you use.

- Set a strong UPI PIN: never your birth year, never 1234, never shared with anyone — not even bank staff. Banks never ask for it.

2. Understand What Each Channel Is For

| Channel | Best for | Daily limit (typical) |

| UPI | Everyday payments, small transfers | ₹1 lakh (₹10 lakh for select categories) |

| IMPS | Instant bank transfers, 24×7 | Varies by bank |

| NEFT/RTGS | Large transfers | ₹2 lakh+ (RTGS) |

| Debit card | ATM cash, POS shopping | Set in your app |

A good rule of thumb from this digital banking guide: UPI for daily life, NEFT/RTGS for big amounts, and turn OFF what you don’t use (international transactions, online card payments) in your bank app.

3. The Golden Safety Rules

- Receiving money never requires your PIN. Anyone who says otherwise is a scammer. This single sentence prevents the most common UPI fraud in India.

- Banks never call asking for OTPs, PINs or card numbers. Ever.

- Don’t click payment links in SMS/WhatsApp — open your app yourself instead.

- Check the name before paying. UPI shows the receiver’s registered name before you confirm — read it.

- Enable transaction alerts and glance at every SMS your bank sends.

The threat landscape changes weekly — bookmark our Cybersecurity section for current scam alerts.

4. Know the 2026 Rules That Protect You

Two rule changes this year make digital banking safer than it has ever been:

- Dynamic 2FA: UPI now requires an extra changing security factor beyond your PIN — see our full explainer on the UPI new rules for 2026.

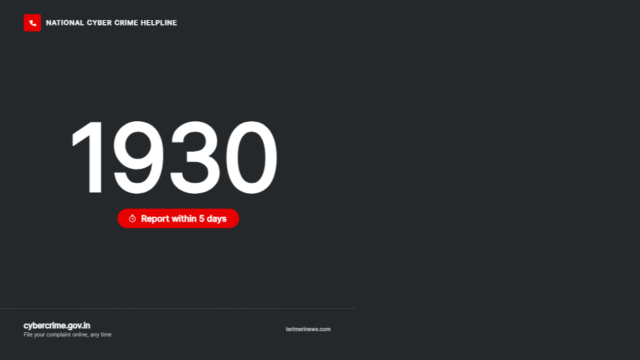

- Fraud compensation: if you’re defrauded despite precautions, the new digital fraud compensation rule can refund up to ₹25,000 — provided you report to your bank and helpline 1930 within 5 days.

Write “1930” on a sticky note near the phone of every senior member of your family. It’s the digital equivalent of knowing where the fire extinguisher is.

5. Build Habits, Not Fear

Digital banking is statistically safer than carrying cash — when used with the habits above. Start small: pay for one week’s groceries by UPI. Check your statement in the app on Sunday. Increase usage as confidence grows. Within a month, the nervousness disappears; the convenience doesn’t.

FAQs

Q1. Is UPI safe for senior citizens?

Yes, with the golden rules above. The biggest risk isn’t the technology — it’s social engineering. Teach the “receiving money never needs a PIN” rule first.

Q2. What if I send money to the wrong person?

Contact your bank immediately and raise a dispute in the UPI app. Recovery depends on the receiver’s cooperation, so always verify the name before confirming.

Q3. Do I need a smartphone for digital banking?

For UPI apps, yes. Feature-phone users can use UPI 123PAY via IVR, and *99# USSD banking works without internet.

Q4. What should I do first if something goes wrong?

Call 1930 (cybercrime helpline) and your bank’s fraud line — within 5 days at most, ideally within the hour.

Disclaimer: General information, not financial advice. Limits and features vary by bank.