Digital Fraud Compensation Rule 2026: Get Up to ₹25,000 Back — If You Act Within 5 Days

Table of Contents

At 9:47 on a Tuesday night, Ramesh Verma, a 52-year-old schoolteacher from Kanpur, got a call from his “bank.” The caller knew his name, his branch, even his last transaction. All he needed was a quick OTP to “block a suspicious debit.” Ninety seconds later, ₹38,000 — half a month’s salary — was gone.

Until last week, Ramesh’s story would have ended there: a police complaint, a few sympathetic shrugs, and a lesson learned at a brutal price. Not anymore — India’s new digital fraud compensation rule has changed the ending.

Under the digital fraud compensation rule 2026, effective July 1, 2026, victims of online payment fraud can now claim back up to ₹25,000, or 85% of their loss (whichever is lower), on losses up to ₹50,000. Ramesh reported his fraud within two days — and his compensation claim is now in process.

There is just one catch, and it is a big one: you must report the fraud within 5 days. Miss that window, and you get nothing.

Here’s everything you need to know — what the rule says, who qualifies, and the exact steps to claim your money back. (Ramesh’s story is an illustrative example based on the most common fraud pattern reported to the 1930 helpline.)

Why the Digital Fraud Compensation Rule Was Desperately Needed: The Numbers

If you have ever felt online fraud is exploding around you, you are not imagining it:

- UPI fraud losses touched ₹1,087 crore across 13.42 lakh cases in FY24, nearly double the previous year, and stayed near ₹981 crore in FY25 (source).

- The RBI’s Annual Report flagged a 34% year-on-year jump in digital payment fraud cases.

- A LocalCircles survey found 1 in 5 families with a UPI user has faced fraud in the last three years — and a shocking 51% of victims never reported it (Business Standard).

- CERT-In has warned that AI-powered scams — cloned voices, fake bank websites, hyper-personalised phishing — are making fraud harder than ever to spot.

Read that 51% figure again. Half of India’s fraud victims stayed silent — because they believed reporting was pointless. The digital fraud compensation rule is designed to change exactly that. When reporting gets your money back, everyone reports. And when everyone reports, fraud networks get mapped and shut down faster.

What Is the Digital Fraud Compensation Rule? (Plain-Language Summary)

| Question | Answer |

| When did it start? | July 1, 2026 |

| Who is covered? | Victims of digital transaction fraud (UPI, net banking, cards) |

| Maximum loss covered | ₹50,000 |

| Compensation | Up to ₹25,000 or 85% of your loss — whichever is lower |

| Deadline to report | Within 5 days — to your bank AND the cybercrime helpline |

| How often can you claim? | One time only — it’s a one-time benefit per person |

Here is the digital fraud compensation rule at a glance — and how the caps work in practice.

Quick math: Lose ₹10,000 → 85% = ₹8,500 back. Lose ₹30,000 → 85% = ₹25,500, capped at ₹25,000. Lose ₹50,000 → capped at ₹25,000.

⚠️ Important: This is not a blank cheque. If you knowingly shared your PIN or participated in the transaction understanding what it was, claims can be rejected. The digital fraud compensation rule protects fraud victims — not negligence. And because it is one-time, treat it as a safety net, not a subscription.

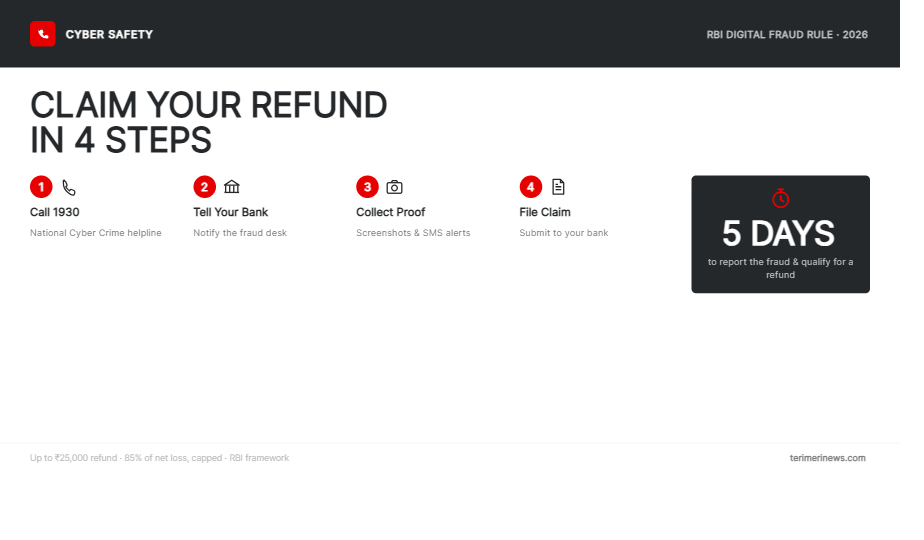

How to Claim Under the Digital Fraud Compensation Rule: 4 Steps

(Insert Image 1 here — step-by-step claim infographic. Alt text: “Digital fraud compensation rule 2026 — 4 steps to claim up to ₹25,000 refund”)

Step 1 — Call 1930 immediately (Day 0)

The moment you spot the fraud, dial 1930, the national cybercrime helpline. Note down your complaint/acknowledgement number — this is your golden ticket. You can also file at cybercrime.gov.in.

(Insert Image 2 here — 1930 helpline graphic. Alt text: “Call 1930 cybercrime helpline within 5 days to claim online fraud refund”)

Step 2 — Inform your bank (within 24 hours ideally)

Call your bank’s fraud helpline, block the compromised card/UPI ID, and register a written complaint. Ask for a complaint reference number. Email a follow-up so there’s a paper trail with a timestamp.

Step 3 — Gather your evidence

Screenshots of the fraudulent transaction, SMS alerts, the scammer’s number/UPI ID, call recordings if any, and both complaint numbers (1930 + bank). The stronger your file, the smoother your claim.

Step 4 — File your claim under the digital fraud compensation rule

Submit the claim through your bank with both complaint references attached. Track it in writing. If the bank stalls beyond a reasonable period, escalate to the RBI Banking Ombudsman (cms.rbi.org.in) — it’s free.

The whole process costs you nothing but 30 minutes. The average UPI fraud costs victims ₹8,000–10,000. That’s the best half-hour ROI you’ll ever earn.

Why the 5-Day Rule Exists

It feels harsh, but there’s logic to it. Fraud money moves fast — through mule accounts, into crypto, out of reach. Banks can freeze funds only while they’re still in the pipeline. Report on Day 1 and there’s a real chance your money is trapped mid-journey; report on Day 20 and it’s gone. The digital fraud compensation rule’s 5-day window forces the one behaviour that actually beats fraudsters: speed.

That’s also why the golden hour matters. Victims who called 1930 within the first hour have historically had the best fund-freezing outcomes. Set this rule in your head today: scam first, panic later — call 1930 first.

Two Scenarios You Should Learn From

The right way: Priya, a 27-year-old Pune IT professional, paid ₹12,000 on a fake “electricity bill disconnection” link. She called 1930 within 40 minutes, filed her bank complaint the same night, and submitted screenshots. Result: her claim for ₹10,200 (85%) is eligible under the digital fraud compensation rule.

The costly delay: Sunil, a retired bank employee — ironically — lost ₹22,000 to a courier-scam call but felt too embarrassed to tell anyone. He reported it on Day 9. Under the new rule, his claim fails the 5-day test. Compensation: zero.

(Both are illustrative composites of the most common patterns in cybercrime complaint data — the embarrassment delay is the single biggest reason victims lose their claim eligibility.)

The difference between Priya and Sunil wasn’t intelligence. It was shame versus speed. Fraud can happen to anyone — bankers, engineers, teachers. The only mistake that actually costs you now is staying silent.

Protect Yourself Before It Happens

The digital fraud compensation rule is your safety net — but prevention still beats compensation:

- Never share OTPs — not with “bank officials,” not with anyone. Banks never ask.

- Turn on transaction alerts and check them.

- Know the new UPI rules for 2026 — limits, 2FA and payment changes.

- Bookmark our Cybersecurity section for scam alerts as they emerge.

- New to digital banking? Start with our banking guides.

1.What is the digital fraud compensation rule?

It’s the new rule effective July 1, 2026, under which online fraud victims can claim up to ₹25,000 or 85% of losses (whichever is lower) on frauds up to ₹50,000 — if reported within 5 days.

2. What is the 1930 helpline?

India’s national cybercrime helpline. Calling it (or filing at cybercrime.gov.in) within 5 days is mandatory for the compensation claim.

3. Is the compensation available every time I’m defrauded

No — it is a one-time benefit.

4. What if I lost more than ₹50,000?

The compensation scheme covers losses up to ₹50,000. For larger amounts, pursue the bank complaint, cybercrime FIR and RBI Ombudsman route — early reporting still maximises fund-freezing chances.

5. Does it cover UPI, cards and net banking?

The digital fraud compensation rule covers digital transaction fraud broadly. Confirm specifics with your bank when filing.

(⚠️ Replace these three URLs with your actual permalinks before publishing — they must be real, live terimerinews.com URLs for Rank Math to count them as internal links. Placeholder text like “INTERNAL-LINK:” is not detected.)